News

4 Benefits of Hyper-Personalisation in Banking

Discover the benefits of hyper-personalisation in banking, from facilitating better resource management to creating bespoke, dynamic and engaging customer experiences.

What can the world of banking learn from digital commerce?

Financial services are changing rapidly. Over the coming years, banks will need to ensure their purpose reflects the expectations of their customers and keeps up with their evolving demands.

Banks and their existing business models face disruption due to challenger and digital banks. Consumers have become used to a certain level of usability, service and customisation – things generally not offered by established financial institutions.

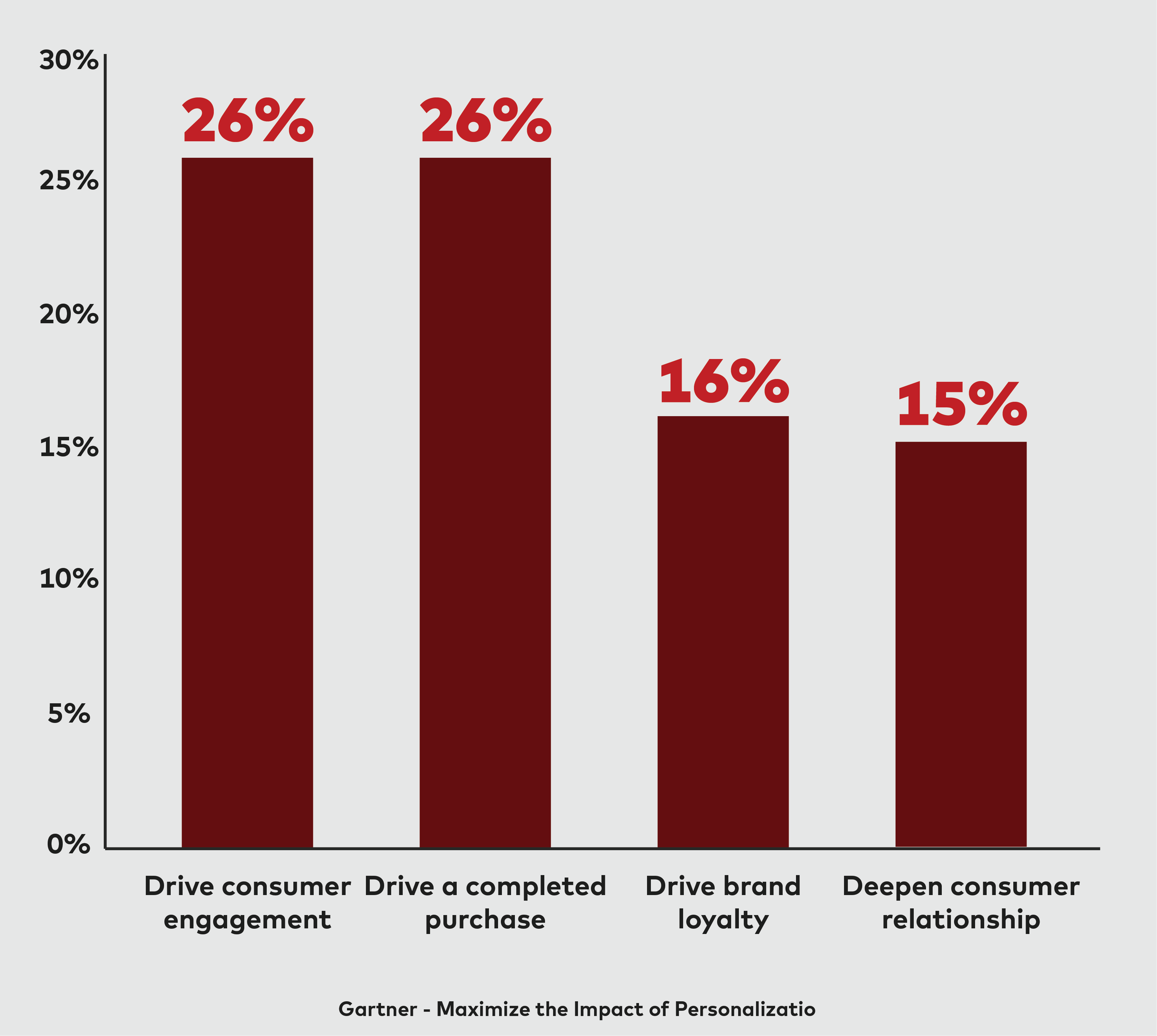

According to Gartner, only 12% of consumers feel brands are meeting their expectations right now vis-à-vis personalisation. However, 16% of product and service providers have already seen more sales than they would have without applying personalisation, proving its inherent value.

But what is hyper-personalisation all about? In what ways can it create truly customer-centric banking experiences? How can it bridge the gap between the financial services and digital commerce worlds? And what are the specific benefits it can offer banks?

What is hyper-personalisation?

Let’s begin with some definitions. Personalisation is something we are all used to. In simple terms, personalisation is the act of customising a product or service directly to an individual user. This could be by addressing a customer by their name in a marketing message.

All well and good so far. But how does hyper-personalisation differ from that?

Hyper-personalisation utilises existing company data in combination with behavioural, contextual and demographic data in real-time, applying AI and machine learning to create an experience, customised to the specific needs of the prospect.

Sounds complex, but from an end-customer’s perspective, it means that a business partner is able to provide targeted and customised offerings to the customer which are extremely relevant at a specific point in time.

Let’s face it: it’s clear why banking is not so different from digital commerce based on this definition. It’s also clear why banks should begin to apply hyper-personalisation to their customer bases who will already be immersed in hyper-personalised retail.

From revenue growth to cost reduction, what benefits can hyper-personalisation bring to a bank?

Customer experience

Customer-centric architecture improvements are arguably the most important benefit of hyper-personalisation. By harnessing real-time data to create interactive and dynamic journeys for customers, they are not just more likely to purchase the product or service in question, but to remain a loyal customer thereafter.

Indeed, hyper-personalisation is more than a nice-to-have; it is at the core of customers’ expectations. A survey of 1,000 adults in the US by Epsilon and GBH Insights showed that 80% of the sample wanted personalisation from retailers. This will naturally translate into demand for similar experiences in financial services, which have become more dependent on digital experiences during the pandemic. For instance, 87% of HSBC’s retail banking transactions are now carried out online.

Resource retargeting

Hyper-personalisation depends on marketing automation – the ability to run data-led campaigns with minimal need for human input. This automation covers not only the personalised elements of a customer’s journey, but the entire sales process.

As well as creating the potential for cost efficiencies, automating processes allows human input to be redirected to the areas which matter: digesting, interpreting and producing incisive insights from data. A private bank in the UK, for instance, used automation as an opportunity to better tailor generic prompts to individual customers’ requests using a decision engine. This boosted customer engagement by 23% and produced a 140% increase in positive outcomes from decisions.

Revenue growth

In order for hyper-personalisation to be successful in financial services, it must naturally deliver strong financials for banks.

This has been the case in the world of digital commerce. Amazon and Netflix have both implemented hyper-personalised customer journeys. Amazon, for example, actively creates personas from data collected from customers’ shopping baskets. If a customer, say, adds a selection of baby products to their basket, this will prompt Amazon to ask the customer the sex of their newborn, incentivising them to buy more by offering the chance to win a Prime subscription. Similarly, Netflix uses customers’ viewing habits – to such a granular level as which parts of films they re-watch or skip – to offer film recommendations.

This approach has boosted revenues for both Amazon and Netflix. 35% and 60% of their sales respectively come from hyper-personalised recommendations. By better tailoring their products and services to what customers need at a specific moment, with pinpoint accuracy, customers are more likely to buy. A lesson that can easily be learned by banks.

Technological innovation

Hyper-personalised banking starts with identifying customer needs. To cook up a solution, one ingredient is needed: data. Whether internal or supplied by a third party, data is at the heart of hyper-personalisation and is essential to achieving any of the above benefits.

As a basis it is extremely important for banks to have a solid data layer and consolidated access to their customer and product data in place. This is so artificial intelligence (AI) can be used to analyse that data and recommend relevant products to specific customers in real-time.

As banks look to the future, new technologies like big data and AI are set to unlock unprecedented potential to improve services and bring institutions closer to customers.

Banks need to place greater focus on new technologies relating to consolidation. Regulation sets banking apart from digital commerce, yet this is likely the largest point of difference. Otherwise, the potential is there in both industries, centring on the core principle of attracting customers to a product or service and then keeping them in the longer term.

Both financial services and digital commerce depend on being able to sell products and services, hence both face the same challenges in this digital age: creating journeys which are seamless, targeted and inspiring.

Find out how Critical can help banks embrace the business opportunities uncovered by managing data correctly by reading our free white paper on Data Consolidation.

Want to chat? Get in touch with Rui Gonçalves who will be delighted to help you hyper-personalise your bank’s customer journey.

We’re also pleased to announce our partnership with Frosmo, specialists in leveraging AI and personalisation to create empowering and timely experiences for businesses to offer their customers.